Loan Management Systems for Banks, SACCOs & MFIs: The Complete Guide (2026)

How a modern loan management system works end to end — origination and intake, credit evaluation and approval, disbursement, document and audit controls, security, and integration — the complete 2026 guide for banks, SACCOs and MFIs.

Lending is a workflow problem before it is a money problem. Between a borrower's first application and the moment funds hit their account sit dozens of steps — data capture, document collection, credit evaluation, approvals, compliance checks, and disbursement — and every one of them is a place where a manual, paper-based process leaks time, introduces errors, and weakens the audit trail.

A modern loan management system turns that chain into a single, traceable digital workflow. This guide is the starting point for everything loan management: how each stage works, where automation pays off, and what banks, SACCOs, and microfinance institutions should look for. Where a topic deserves more depth, we link to a dedicated article.

What a loan management system does

A loan management system (LMS) digitises the full loan lifecycle — origination, underwriting, approval, disbursement, and the audit record that ties them together — on one platform with role-based access and a complete history of every action. The payoff is faster decisions, fewer errors, and the kind of end-to-end traceability regulators and auditors expect. The platform view is set out in Supporting Business and Individual Loans Under One Roof and Data-Driven Loan Intelligence.

Loan origination and intake

Origination is where speed and data quality are won or lost. Digitising intake — structured application forms, mobile-friendly capture, and self-service document upload — removes the re-keying and chasing that slow down paper processes:

- Digitizing Loan Intake: The First Step to Smarter Lending

- Streamlined Application Intake and Fast Application Submission

- Seamless Document Collection for Loan Applications and Mobile-Friendly Uploads for Field Operations

- Digital Co-Applicant and Guarantor Flows and How to Capture Accurate Borrower Data for Loan Risk

Credit evaluation and approval

This is the heart of the system: turning an application into a defensible credit decision through structured proposals, risk assessment, and multi-level approval workflows that route the right cases to the right people:

- Credit Evaluation Microservice and Proposal Preparation in the Credit Proposal Workflow

- Custom Approval Workflows for Lending and Internal Decision Accuracy via MCC Review

- Risk Assessment for Large Loans and Governance & Compliance in Workflow Automation

- Faster Loan Approvals with Real-Time Document Uploads, Seamless Credit Workflow Transitions, and Workflow Automation & State Machines

Disbursement

Once approved, disbursement should be automatic, controlled, and logged — triggered by the workflow rather than a manual hand-off. See Smooth Loan Disbursement and the event-driven Disbursement Trigger Microservice.

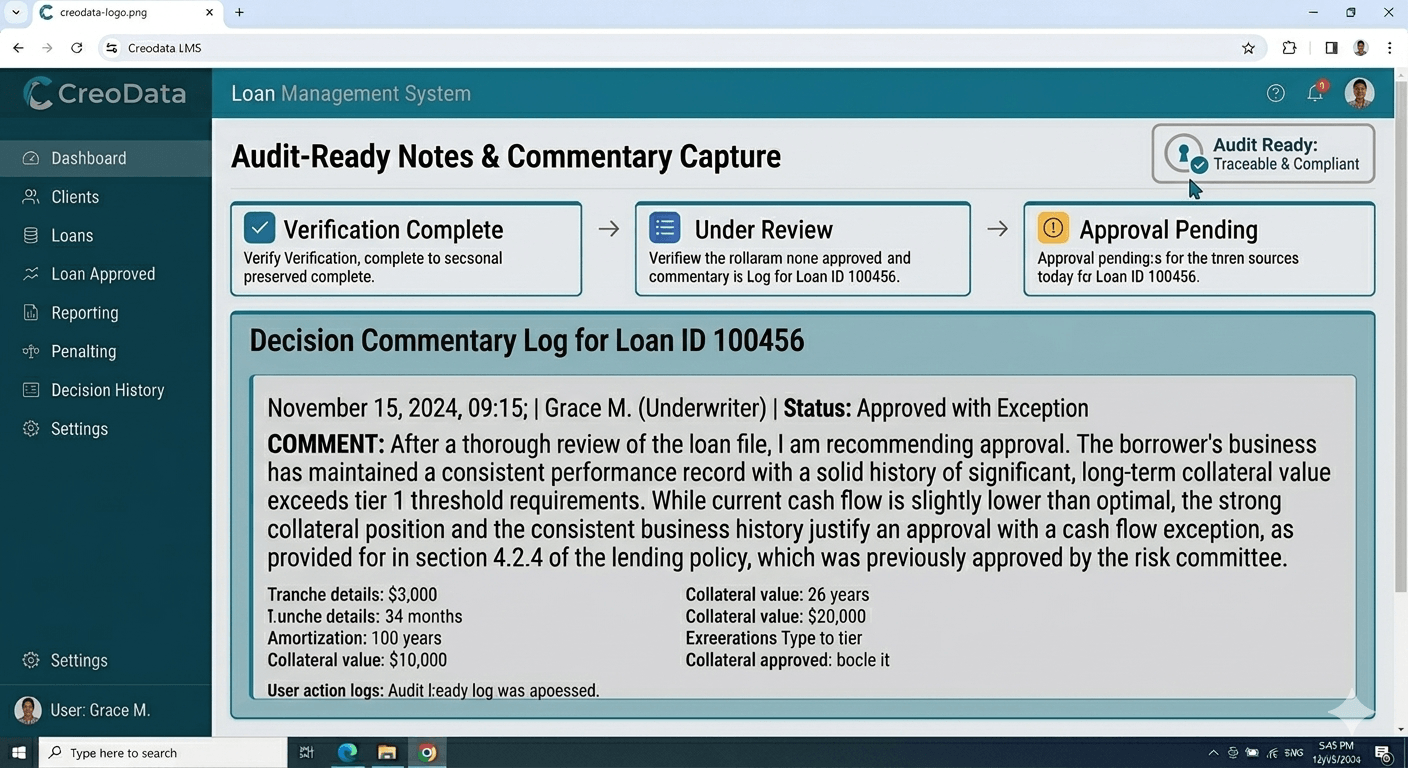

Documents, verification, and audit readiness

Lending generates a mountain of documents, and their integrity is what makes a loan defensible later. Automated validation, metadata, and immutable history logs turn that mountain into an asset:

- Auto-Validation of Uploaded Documents and Automated Document Verification

- How Loan Document Metadata Enables Audit Readiness and Document Upload as a Service

- Audit-Ready Event Logs, Regulatory-Ready History Reporting, Time-Stamped Application Audits, and Internal Audits Made Easy with History Logs

Security, roles, and oversight

Lending data is sensitive, and access must be tightly governed by role — with dashboards that give each function the oversight it needs:

- Azure AD for Loan Security and Role-Based Assignment

- User Action Traceability in Loan Workflow and BM Tracking: Loan Workflow Visibility and Control

Integration, automation, and scale

A loan platform delivers most when it connects to your core banking system and scales with volume — using cloud-native architecture rather than brittle batch jobs:

- Connecting to Core Banking Systems and Automated Loan Processing via Azure

- Scaling Loan Operations Efficiently and the real-time view in Real-time Application Status Updates and Instant Loan Application Notifications

Choosing a loan management platform

Creodata's Loan Management System brings origination, document collection, credit evaluation, multi-level approvals, and disbursement together on a secure, Azure-hosted platform built for banks, SACCOs, and MFIs across the region. Book a demo to see it against your own lending workflow.

Frequently asked questions

What is a loan management system?

A loan management system is software that digitises and automates the full loan lifecycle — application intake, document collection, credit evaluation, approval, disbursement, and the audit record — on a single platform. It replaces fragmented spreadsheets, email, and paper with one traceable workflow, which speeds up decisions and strengthens compliance.

How does a loan management system speed up approvals?

It removes the delays built into manual lending: applications and documents are captured digitally and validated automatically, proposals and risk assessments are structured and consistent, and approval workflows route each case to the right approver with no physical hand-offs. Real-time status tracking means nothing sits idle waiting for someone to notice it.

Is a loan management system suitable for SACCOs and microfinance institutions, not just banks?

Yes. The same origination, approval, and audit controls apply whether you are a commercial bank, a SACCO, or a microfinance institution — and a good platform supports both individual and group lending. Cloud hosting and per-use pricing make enterprise-grade lending automation accessible to smaller institutions without a large up-front investment.

How does a loan management system support audit and compliance?

Every action — who submitted, reviewed, approved, or changed a record, and when — is logged immutably, and documents carry metadata that makes them easy to locate and verify. This produces a complete, time-stamped history that can be reported to auditors and regulators on demand, rather than reconstructed after the fact.

This is the hub for Creodata's loan management coverage. Explore the linked guides for depth on origination, credit workflows, disbursement, audit, and integration — or see the Loan Management System in a demo.