Credit Evaluation Microservice

Isolate credit evaluation in a dedicated microservice for faster, fairer, and auditable lending decisions that scale with modular loan-management architecture.

Modern lending platforms need to make faster, fairer, and auditable credit decisions while remaining flexible to change. Embedding credit evaluation into a small, well-scoped microservice — the EvaluateCreditworthinessFn — is a practical way to achieve that. This article explains what that function should do, how it fits into a modular loan-management system, the architecture and design patterns to follow, and the operational, compliance, and product advantages — with concrete references to CreoData's Loan Management platform features and target audience where relevant.

Why Isolate Credit Evaluation into Its Own Function?

Separating credit evaluation into a single-purpose microservice follows the single-responsibility principle and yields multiple practical benefits:

-

Clear ownership and governance: The credit-scoring logic, input validation, and audit trails live in one deployable unit, simplifying reviews and approvals.

-

Independent scale and latency control: Credit scoring can be CPU- or model-heavy; scaling it separately avoids over-provisioning other parts of the loan pipeline.

-

Faster iteration and model experimentation: Teams can test new scoring models or features without touching onboarding, repayment, or accounting services.

-

Safer upgrades and compliance-friendly change management: When scoring models change, a confined surface area reduces regulatory and QA burden.

These ideals align with the design of cloud-native loan management platforms — for example, CreoData's Loan Management product emphasizes configurable workflows, onboarding, and approval hierarchies that are well suited to integrating dedicated services for tasks like credit assessment.

Functional Responsibilities of EvaluateCreditworthinessFn

At its core, the function should receive borrower and application context and return a deterministic, auditable evaluation that downstream services can act on. Typical responsibilities:

1. Ingest and Normalize Data

- Customer profile (identity, KYC status, income, employment)

- Application details (loan amount, term, product code)

- Historical behavior (payment history, existing exposures)

- External scores and bureau data (when available)

- Alternative data (transaction history, device or mobile indicators, if allowed)

2. Apply Pre-Processing Rules

- Required-field validation and simple business-rule checks (e.g., minimum age, KYC pass/fail).

- Missing-data strategies (imputation, reject/triage).

- Data transformations required by models (feature engineering).

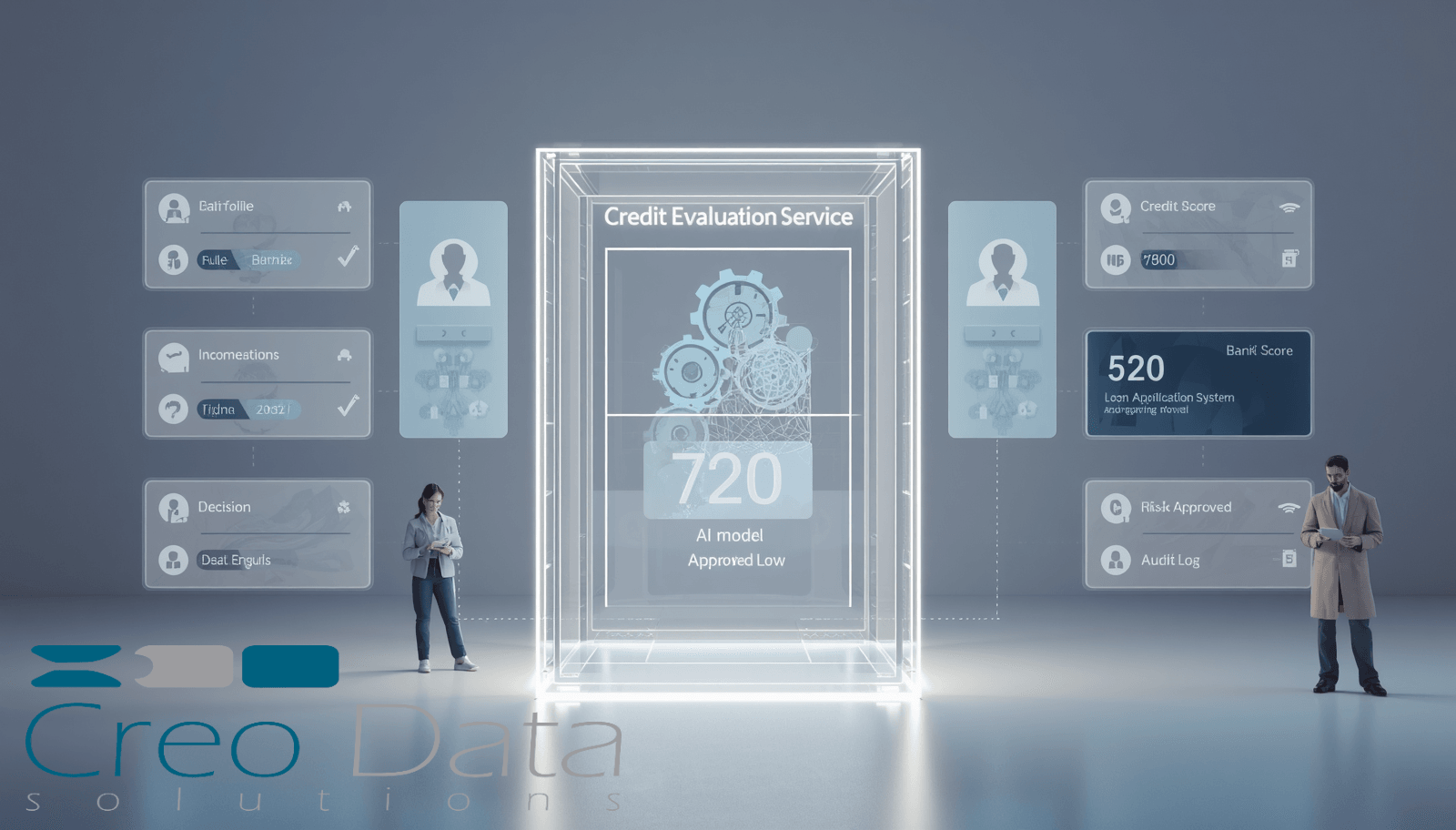

3. Compute Risk Scores

- Run deterministic rules (hard declines, policy flags).

- Run statistical or ML models (probability of default, propensity).

- Produce score breakdowns (which features contributed most) for explainability.

4. Produce Decision Artifacts

- Numeric score(s) + band/grade (e.g., A–D).

- Decision recommendation (approve, refer to manual review, decline).

- Confidence/uncertainty metrics.

- Audit metadata (model version, input snapshot, timestamp, request id).

5. Expose Interfaces

- Synchronous API (REST/gRPC) for origination flows.

- Asynchronous message topics (events) for batch scoring or model retraining triggers.

- Admin endpoints for retrieving logs, score explainability info, and model metadata.

6. Support Extensions

- Plug-in model registry (A/B test models).

- Customizable business rules per product or customer segment.

- Feature toggles for experimental scoring features.

Architecture & Integration Patterns

1. Bounded Context & Data Ownership

Treat the credit evaluation microservice as the authoritative source for scoring decisions. It should not own full customer records but should cache read-only snapshots derived from the canonical customer store. This keeps ownership boundaries clear and avoids duplication of write logic.

2. Model Hosting and Versioning

Keep models in a model registry; the service references models by immutable version IDs. Record the model_version in the audit artifact for traceability and regulatory reporting. This also enables A/B testing: route a portion of traffic to a new model version while recording comparative outcomes.

3. Rules Engine vs. ML Models

A hybrid approach is practical. Implement deterministic rules in a rules engine (fast, explainable) and machine-learning models for nuanced probability estimates. The microservice composes these sources into a final decision (e.g., rules can hard-decline or override model output for policy compliance).

4. Observability and Explainability

Score explanations (feature contributions, flags triggered) should be part of the response and stored in the system's audit logs. Instrument the service with:

- Structured logging (JSON) including request id and model id

- Tracing (distributed tracing spans) to follow the evaluation within a loan origination flow

- Metrics: latency, QPS, model inference time, score distributions

These capabilities align with CreoData's loan-management platform capabilities like real-time reporting and support for multi-level approval workflows, which expect decision artifacts and explainability to drive approvals and committee reviews.

Data Privacy, Compliance, and Fairness

Credit evaluation touches sensitive data and outcomes that can materially affect customers. The microservice must:

-

Log minimally: Store only what's required for audit and dispute resolution; redact PII where unnecessary.

-

Retain audit trails: Keep full evaluation artifacts — inputs, model id, outputs — for the regulatory retention window.

-

Support explainability: Present human-readable reasons for adverse actions; include model version and feature contributions.

-

Bias monitoring: Track score distributions by protected attributes (if legally and ethically permitted) and conduct periodic fairness audits.

-

Consent & data sourcing: Ensure external data (bureaus, alternative data) is used in accordance with consent and local regulations.

CreoData's product framing around secure onboarding, KYC capture, and audit-ready workflows makes it a natural host for a service that must enforce strict governance and retention rules.

Scalability, Performance and Reliability

-

Autoscaling: Separate compute for inference enables scaling up for heavier model loads without affecting other services.

-

Caching: Cache common external bureau lookups for short windows to reduce latency and cost (while respecting freshness requirements).

-

Circuit breakers and fallbacks: If external scoring services or models fail, provide predefined fallback recommendations or fail-open/close according to business rules.

-

Bulk/batch scoring: Support scheduled batch evaluation for portfolio re-scoring (e.g., monthly debt servicing checks) via background jobs or an event-driven consumer.

CreoData's cloud-native approach and Azure deployment options mean hosting and scaling these microservices is operationally feasible for the intended customers, including small banks and microfinance institutions.

Extendibility & Productization: Making EvaluateCreditworthinessFn Future-Ready

Design the function so lenders can adapt it to their products and risk appetite:

-

Per-product parameterization: Allow threshold, weight, and rule overrides by product code (e.g., payroll loans vs. asset loans).

-

Custom rule plugins: Support institution-specific rules (e.g., guarantor acceptance, group-lending heuristics).

-

Model plugin interface: Enable pluggable model runners (e.g., scikit-learn, ONNX, TensorFlow Serving) via a standard adapter so data scientists can bring their own models.

-

Dashboard & governance UI hooks: Surface score distributions, flagged cases, and model performance metrics to risk teams. CreoData's loan-management UI and workflow tooling already provide places to attach such governance controls and MCC (multi-level credit committee) review workflows.

Advantages (Business & Technical)

1. Faster, Consistent Decisions

Compact, purpose-built scoring reduces latency and centralizes scoring policies — approvals can be automated for low-risk cases while higher-risk cases are routed to committees.

2. Better Risk Control

Centralizing scoring and versioning limits accidental drift and makes portfolio-level monitoring straightforward.

3. Regulatory & Audit Readiness

By storing evaluation artifacts with model versions and explainability details, the service lets lenders respond to audits and disputes quickly. (This maps to CreoData's emphasis on audit-ready workflows and reporting.)

4. Product Extensibility

Plug-in rules and models let institutions launch new lending products and iterate on risk policies without large reworks.

5. Operational Efficiency

Offloading scoring to a separate service reduces the operational complexity of other components and streamlines testing and deployment.

Target Audience

EvaluateCreditworthinessFn is valuable to a range of financial and lending organizations:

-

Small & mid-sized banks seeking configurable, auditable scoring to support digital loan origination.

-

Microfinance institutions & SACCOs that require field-friendly onboarding and rapid yet compliant scoring (especially in mobile-first contexts).

-

Fintech lenders / digital credit providers that iterate rapidly on models and need safe A/B experimentation.

-

Credit unions and cooperative societies that want product-level control (group loans, individual loans, variable collateral rules).

These are the same segments Creodata's Loan Management solution targets — cloud-native, Azure-based, and built to support onboarding, KYC capture, and configurable approval hierarchies.

Implementation Checklist (Practical Steps)

- Define minimal viable input/output (I/O) contract and version it.

- Select model hosting strategy (in-service lightweight model vs. dedicated model server).

- Build rule engine for hard policies to run before/after ML models.

- Implement auditing & explainability primitives (store inputs, outputs, model id, reasons).

- Add metrics & tracing: latency per call, score distribution, model inference time.

- Create admin UI hooks to view scoring outcomes, distributions, and flagged cases.

- Design for testing: unit tests for rules, back tests for models, integration tests across the origination flow.

- Plan deployment & rollout: feature flags, canary traffic, and A/B test scaffolding.

Conclusion

A focused EvaluateCreditworthinessFn microservice is a modular, practical way to make credit decisions that are fast, auditable, and adaptable. By encapsulating scoring logic, model versioning, and explainability in a single bounded context, lenders reduce operational complexity and increase governance and product velocity. Paired with a cloud-native loan management platform — like CreoData's Loan Management system with its configurable workflows, onboarding, and reporting — such a microservice becomes a powerful building block for modern lending operations.

For more information, visit Creodata.com