Workplace Banking for Lenders: The Complete Guide to Check-Off Loan Origination (2026)

The complete guide to workplace-banking (check-off / scheme) lending — the unsecured loan origination lifecycle end to end, from employer schemes, affordability and calculators to compliance, the multi-stage workflow, disbursement, SLAs, audit and core-banking integration.

Workplace banking — sometimes called scheme banking or check-off lending — is the practice of extending unsecured personal loans to salaried employees and recovering the repayments directly from payroll. Instead of relying on collateral, the lender relies on the employer's payroll deduction (the "check-off") and a verified, recurring salary. For banks, SACCOs and microfinance banks across Kenya and East Africa, it is one of the most predictable retail lending books available, because repayment is deducted at source before the borrower sees their net pay. This guide is the starting point for understanding how that lending model works end to end, and how a purpose-built origination platform supports each stage. It draws on the design of the Creodata Workplace Banking platform (WPB) — eleven independently deployable .NET 9 Azure Functions microservices behind a Next.js portal — but the lifecycle it describes is the same one every check-off lender has to run, whether on paper or in software.

If you are new to the model, two companion articles set the foundations: what workplace banking is and why lenders run it, and a closer look at how check-off loans work in Kenya, including the role of the employer and the payroll deduction itself. The rest of this guide walks the lifecycle in the order a lender actually experiences it, and at each stage points to a focused article that goes deeper.

Why lenders digitise check-off lending

On paper, check-off lending looks simple: a salaried customer applies, the lender checks affordability, deducts an instalment from payroll, and books the loan. In practice it is a long chain of dependent steps — employer onboarding, affordability calculation, identity and credit checks, document collection, credit analysis, approval, booking and disbursement — each owned by a different role, each governed by policy and regulation, and each a place where time and money leak. Manual processing means inconsistent affordability sums, lost documents, slow turnaround, weak audit trails, and approval decisions that are hard to defend to a regulator or an internal auditor.

Digitising the process is about making that chain consistent and traceable. A good origination platform enforces the same affordability policy on every application, runs the same compliance checks, routes work to the right role at the right time, and records who did what and when in an immutable trail. WPB does this through purpose-built services — EmployerScheme, LoanCalculator, LoanApplication, WorkflowEngine, Compliance, Document and Disbursement, plus Authorization, Auditing, EmailNotification and SLAMonitoring — so that every loan follows the same defensible path. This is distinct from generic loan management — covered in our loan-management complete guide — which handles the lifecycle of a loan once it is on the books. Workplace banking is specifically about originating the unsecured, payroll-deducted facility correctly in the first place.

The set-up layer: employer schemes and parameters

Check-off lending begins before any customer applies. The lender must first onboard the employer and define the scheme under which its staff can borrow. An employer scheme captures who the employer is, which allowances and deductions appear on its payslips, and the lending parameters that apply to its employees. In WPB this is the job of the EmployerScheme service, which manages employer and scheme records, allowance and deduction types, and the scheme parameters themselves.

Once a scheme is selected during an application, a fixed set of parameters governs every loan written against it:

| Scheme parameter | What it controls |

|---|---|

| Interest rate | The rate applied to loans under the scheme |

| Minimum and maximum loan amount | The lending band the employer's staff may borrow within |

| Processing fees | Origination fees recovered at disbursement |

| Minimum and maximum tenure | The repayment-period band |

| Insurance amount payable | Credit life cover premium |

Getting this layer right is foundational — every downstream calculation, affordability check and approval inherits these values. Our guide to employer scheme onboarding for workplace lending covers how to structure schemes, maintain allowance and deduction variables, and handle the difference between government ministries (whose deductions are booked through IPPD) and private employers.

The pre-sale layer: affordability and the three calculators

Before a customer formally applies, a Direct Sales Executive runs the numbers. This pre-sale layer is where the LoanCalculator service does its work, and it offers three distinct tools:

- A forward calculator that takes a loan amount and returns the equated monthly instalment (EMI) and repayment.

- A reverse calculator that takes a desired monthly repayment and returns the maximum loan amount it supports.

- An affordability check that derives a customer's maximum borrowing capacity from their payslip. The user selects the employer, and the calculator factors in all of that scheme's allowances (House, Commuter, Hardship, Other) and deductions (PAYE, NSSF, NITA, NHIF, provident/pension, SACCO contributions and loans, bank loans, other loans, reimbursements).

A central policy applies throughout: a minimum take-home of KES 50,000 must remain after the new instalment. This is a bank-configurable figure, and it holds even where the customer is buying off another loan — and any loan being taken over must be included in the affordability sum so the calculation reflects the customer's true position once the buy-off completes. For example, a customer earning KES 120,000 with existing deductions can only borrow up to the point where their net pay still clears that KES 50,000 floor. The mechanics of the affordability check from a payslip and the workings of the forward, reverse and affordability calculators each have a dedicated article.

Product types, including buy-off / takeover

Workplace banking covers three loan types: a New Loan, a Top-up on an existing facility, and a Buy-Off / Take Over where the lender settles a customer's loan at another institution and replaces it with its own. Buy-offs are eligible against facilities at any bank licensed by the Central Bank of Kenya, any CBK-licensed microfinance bank, any SACCO, and microfinance institutions approved by the lender.

Buy-offs follow a different path through the workflow and through disbursement — takeover funds route to a suspense account, settlement to another bank goes via RTGS, and settlement to a SACCO credits a branch suspense account with a bankers cheque issued to the branch. The final takeover disbursement only releases on a certified loan statement showing a nil balance or a clearance letter from the other institution, plus confirmation that the old check-off has been stopped. The full mechanics are covered in the loan buy-off and takeover process.

The 13-stage workflow and credit analysis

Every application moves through a structured workflow with role-based authorisation and decision gates at each stage. The WorkflowEngine enforces who can act, what actions are available, and where the application goes next. The thirteen stages run in this order:

- Pre-Sale Calculation — Direct Sales Executive (DSE)

- Customer Application — DSE

- Document Collection — DSE

- Application Review — Sales Manager

- Document Verification & Data Capture — Sales Centre Compliance Analyst (SCCA)

- Credit Analysis — Credit Analyst

- Credit Approval — Credit Approver

From approval, the path branches by product type. New loans and top-ups go to Check-Off Booking (Scheme Loan Administrator), then Loan Booking, Disbursement, Post-Disbursement and Completed. Buy-offs go to Loan Booking, then a Buy-Off Clearance stage with the SCCA, then Loan Booking, Disbursement and Completed. At each stage the available actions are Comment, Forward/Recommend, Return (with reason), Decline (with reason), Approve (reserved for the Credit Analyst and Credit Approver) and Refer (at the check-off and booking stages). Standard decline and return reasons are maintained as a dropdown alongside free-text.

The heart of the decision sits at stage six, where the Credit Analyst assesses the application against the lender's policy. Our article on credit analysis for unsecured personal loans explains how the analyst works, and the full workplace-banking loan workflow walks all thirteen stages, the ten roles and the decision gates in detail.

The compliance spine

Compliance runs alongside the workflow rather than as a single gate. The Compliance service performs external checks through integration adapters — IPRS for national ID and passport verification (which also auto-populates bio-data), CRB for credit reference, KRA for tax PIN verification, and Comply Advantage for AML, sanctions and PEP screening — each result cached for 24 hours. Alongside these sits a deterministic business-rules engine (not machine learning): the PEP check, the KES 50,000 minimum take-home, a retirement-age rule (loan maturity must not exceed three months before retirement), debt-to-income and one-third-of-basic-salary tests, CRB rules, an employment-contract-maturity rule, an existing-facilities check and net-pay verification against bank-statement credits. Reviewers work from a split screen showing the application beside every search result.

Employee verification adds a further control: employers confirm employment through an agreed channel (a recorded telephone line or email), with the contact, date and time recorded. Government ministries are exempted at the credit stage because the call-back has already happened in sales, while private employers receive it as enhanced due diligence. The origination checks are explained in compliance checks in loan origination in Kenya. For ongoing transaction monitoring and the deeper screening engine — including sanctions and PEP screening, the customer risk-assessment model and enhanced due diligence — those responsibilities belong to the dedicated AML compliance platform and its complete guide, with advisory support available through financial-crime compliance services.

Documents, OTP, booking and disbursement

Document collection is checklist-driven, and the matrix differs for customers existing at the bank versus those new to it. The Document service handles upload, download and verification through a storage abstraction, and auto-generates the Check-Off Authorization Form. Once documents are in, the system auto-generates a loan offer for the customer to execute and upload, sends a one-time password (OTP) by SMS with a link to the loan and account-opening terms, and regenerates the OTP if any customer or loan detail changes after verification. A reference number and DSO code are assigned automatically. The full list — pay slips, IDs, KRA PIN, employment contracts, buy-off loan statements and more — is set out in the loan application documents checklist for Kenya.

Booking and disbursement are where the loan becomes real. The Disbursement service books the loan in Finacle, marks limits, and disburses (full, partial or final). Dual control is enforced by a database constraint so the inputter and verifier must be different users — the principle behind maker-checker loan disbursement. For new-to-bank customers, a CIF and transactional account are auto-created in parallel with the loan workflow, where origination hands off to business account opening and its complete guide. A one-month moratorium applies, the first instalment falls due on the 10th of the month after it expires, and break-period interest is calculated daily and paid monthly where the gap exceeds a month. The mechanics of loan booking and disbursement through the core banking system cover Finacle booking fields, fee recovery and repayment-schedule amendments in full.

Operations and platform: SLA, audit and integrations

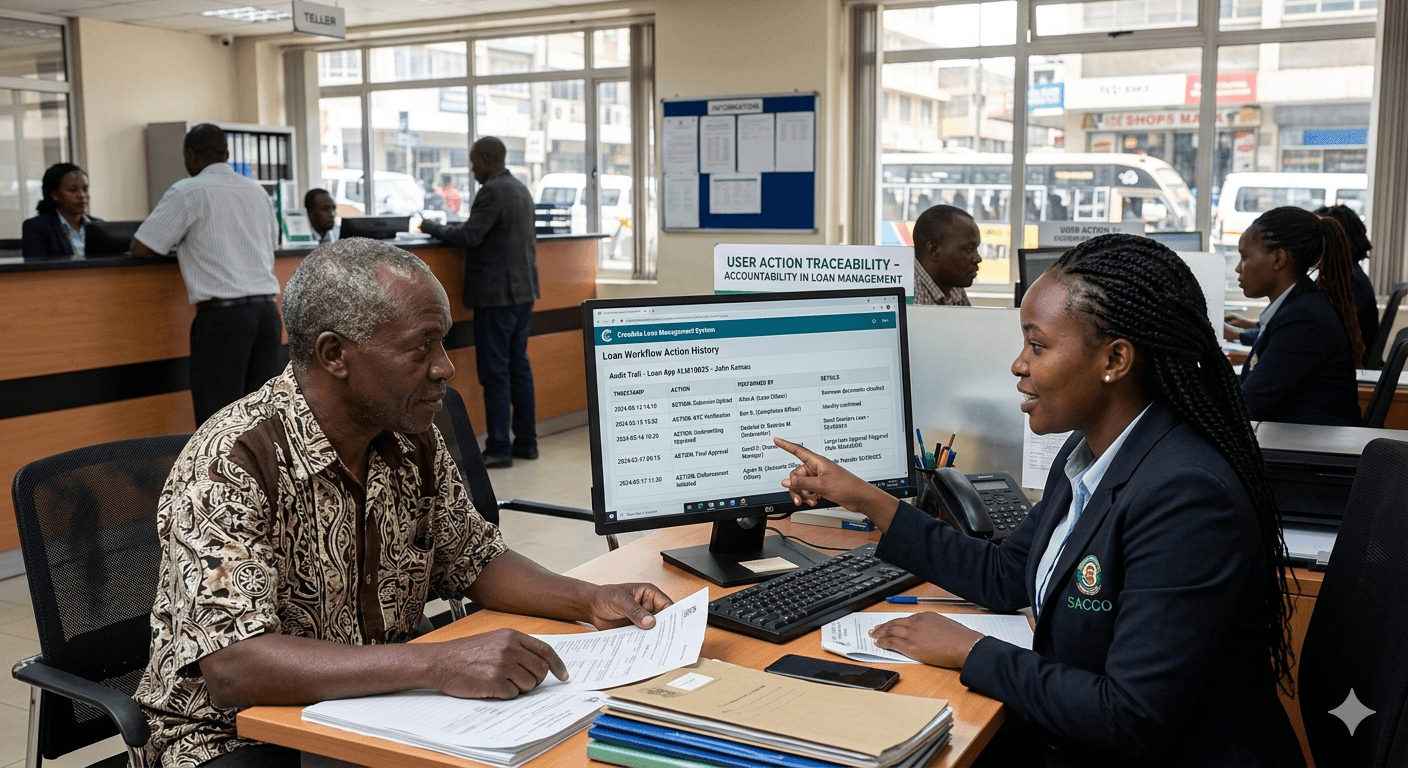

Three platform capabilities run underneath every loan. The SLAMonitoring service configures a time limit per workflow stage, tracks start and completion, detects breaches and produces turnaround-time (TAT) reports — covered in loan processing turnaround time and SLAs. The Auditing service writes to an immutable audit log (a database trigger blocks updates and deletes), and the Authorization service enforces role-based access across ten roles and twenty-one permissions; both are explained in audit trail and RBAC for a lending platform. And the whole platform connects outward through an adapter-based integration layer — Finacle, IPRS, CRB, KRA, Comply Advantage, IPPD, DMS, RTGS, SMS and email — each wrapped in Polly retry and circuit-breaker resilience, as described in workplace-banking system integrations.

The table below maps the lifecycle to what a lender needs at each stage and how the platform supports it.

| Lifecycle stage | What the lender needs | How WPB supports it |

|---|---|---|

| Set-up | Employer schemes and lending parameters | EmployerScheme service: scheme CRUD, allowance/deduction types, parameters |

| Pre-sale | Consistent affordability and pricing | LoanCalculator: forward, reverse and affordability, KES 50,000 take-home floor |

| Application | Capture, OTP and documents | LoanApplication and Document services; OTP, reference number, checklist |

| Decision | Compliance and credit analysis | Compliance service (external checks + business rules); WorkflowEngine credit gates |

| Booking | Dual-controlled disbursement | Disbursement service: Finacle booking, maker-checker, moratorium handling |

| Operations | Turnaround, audit and access control | SLAMonitoring, Auditing (immutable log), Authorization (RBAC) |

WPB ships as either an Azure Marketplace managed application deployed to the bank's own subscription or an on-premises Kubernetes deployment, with feature parity between the two. Telemetry, messaging, storage and authentication backends switch by environment variable, so the same product runs in the cloud or in your own data centre.

Frequently asked questions

What is the difference between workplace banking and ordinary personal lending?

Ordinary personal lending typically relies on the borrower making repayments from their own account, often against some form of security or a general affordability assessment. Workplace banking is unsecured but repaid through a payroll check-off: the employer deducts the instalment at source before the employee receives their net pay, under a scheme the lender has agreed with that employer. This changes the entire origination flow. It adds an employer-scheme set-up layer, an affordability calculation built from specific payslip allowances and deductions, employee verification with the employer, and check-off booking. The repayment risk profile is therefore tied to the employer relationship and the payroll deduction, not to collateral.

Does the platform run in our own data centre or only in the cloud?

Both, with feature parity between them. WPB can be deployed on-premises on Kubernetes, or as a transactable Azure Marketplace managed application that a bank installs into its own Azure subscription through a one-click wizard, with the publisher retaining read-only support access. The architecture is designed so the same code runs in either environment: the telemetry, messaging, storage and authentication backends are selected by environment variable through interface-based dependency injection — OpenTelemetry and Prometheus or Azure Application Insights, RabbitMQ or Azure Service Bus, MinIO or Azure Blob Storage, Keycloak/LDAP or Azure AD. Secrets live in Kubernetes Secrets on-premises or Azure Key Vault in the cloud. The choice is yours to make based on your existing infrastructure and data-residency requirements.

How does WPB relate to the AML and loan-management products?

They are complementary. WPB is the origination platform: it takes an unsecured check-off loan from pre-sale calculation through to disbursement, and includes the compliance checks needed at origination — IPRS, CRB, KRA and Comply Advantage screening plus a deterministic business-rules engine. Ongoing AML responsibilities — continuous transaction monitoring, the deeper screening engine, customer risk assessment and enhanced due diligence — sit with the separate AML compliance platform. And once a loan is booked and live, its servicing lifecycle is the domain of generic loan management. WPB focuses on originating the workplace-banking facility correctly and handing it off cleanly to those neighbouring systems.

To see the full origination lifecycle in one place, explore the Workplace Banking product page, and when you are ready to walk it through with your own scheme parameters and policy, book a demo or get in touch.