Loan Application Documents and the OTP-Signed Offer: A Lender Checklist

The documents a workplace-banking loan needs in Kenya — the existing-vs-new-to-bank checklist, payslip and salary-statement rules, the auto-generated offer, OTP e-acceptance and the check-off authorization form.

Documentation is where a workplace-banking loan either firms up into a clean, bookable facility or stalls in a queue of missing pages and uncertified payslips. In a check-off (payroll-deduction) lending operation, the document step sits between the customer application and the credit decision: it is the point at which the lender assembles the evidence that the applicant is who they say they are, earns what they claim to earn, and has authorised the employer to deduct repayments at source. Get the checklist right and the file moves smoothly through verification, credit analysis and booking. Get it wrong and the same file bounces back from the Sales Centre Compliance Analyst (SCCA) or, worse, from credit. This article walks through the documentation matrix the Workplace Banking (WPB) platform enforces, how upload and verification work, and how the auto-generated loan offer is signed by the customer through a one-time-password (OTP) flow. It is part of the complete guide to workplace banking; for the decisioning that happens once the documents are in, see credit analysis for unsecured personal loans.

The documentation matrix: existing versus new to bank

The single most important distinction in workplace-banking documentation is whether the applicant is an existing customer of the bank or new to the bank. An existing customer whose salary already lands in a Finacle account does not need to prove their salary credits with stamped statements — the core banking system already shows them. A new-to-bank applicant has no such trail inside the bank, so the documentary burden is higher and includes salary credit statements that must be authenticated by a call-back to the paying institution.

WPB models this as a checklist-driven documentation matrix that differs between the two cohorts. The table below sets out the standard items and where each applies.

| Document | Existing customer | New to bank |

|---|---|---|

| Application Form & Terms and Conditions | Required | Required |

| Copy of National ID or Passport | Required | Required |

| Latest pay slip (certified by an authorised signatory) | Required | Required |

| Employees Check-Off Authorization Form | Required | Required |

| KRA PIN | Required | Required |

| Salary credit statements | Not needed if salary credits are evident in Finacle | Original latest 3 months, stamped and signed, with a call-back to authenticate |

| Employment contract (contract staff, certified) | Required for contract staff | Required for contract staff |

| Letter of undertaking / work permit (expatriates) | Required for expatriates | Required for expatriates |

| Recent passport-size photograph | Required | Required |

| Loan statement (buy-offs only, stamped and signed by the other lender) | Required for buy-offs | Required for buy-offs |

| Account Opening Form | Only if no account exists | Required (no account yet) |

A few of the rules behind that matrix deserve emphasis, because they are where files most often come unstuck:

- Pay slip certification and consistency. The latest pay slip must be certified by an authorised signatory. Where salary is inconsistent month to month, the lender takes the latest three months; where income is commission-based, it takes six months and holds cash security against the commission income. These rules protect the affordability assessment — for the mechanics of that calculation, see the payslip-based affordability check.

- Salary credit statements and the call-back. For a new-to-bank applicant, the original latest three months of salary statements are required, stamped and signed, and the lender performs a call-back to the paying institution to authenticate them. For an existing customer, this is unnecessary when Finacle already shows the salary credits.

- Contract staff and expatriates. Contract staff supply a certified employment contract; expatriates supply a letter of undertaking or work permit. These feed directly into the contract-maturity rule applied at credit, which prevents a tenure that runs past the contract or permit expiry.

- Buy-offs. A take-over needs a loan statement from the institution being bought off, stamped and signed by that lender, so the settlement figure is documented. The end-to-end mechanics are covered in the loan buy-off and take-over process.

Checklist-driven upload and verification

The Document service in WPB drives this matrix as a live checklist rather than a static form. As the application is built, the relevant items appear for that applicant — existing or new to bank, salaried or commission-based, permanent, contract or expatriate, new loan or buy-off — and each can be uploaded against its checklist line. Files are held through a storage abstraction that uses MinIO on-premises or Azure Blob Storage in the cloud, so the same upload and download behaviour applies regardless of where a given bank has chosen to deploy.

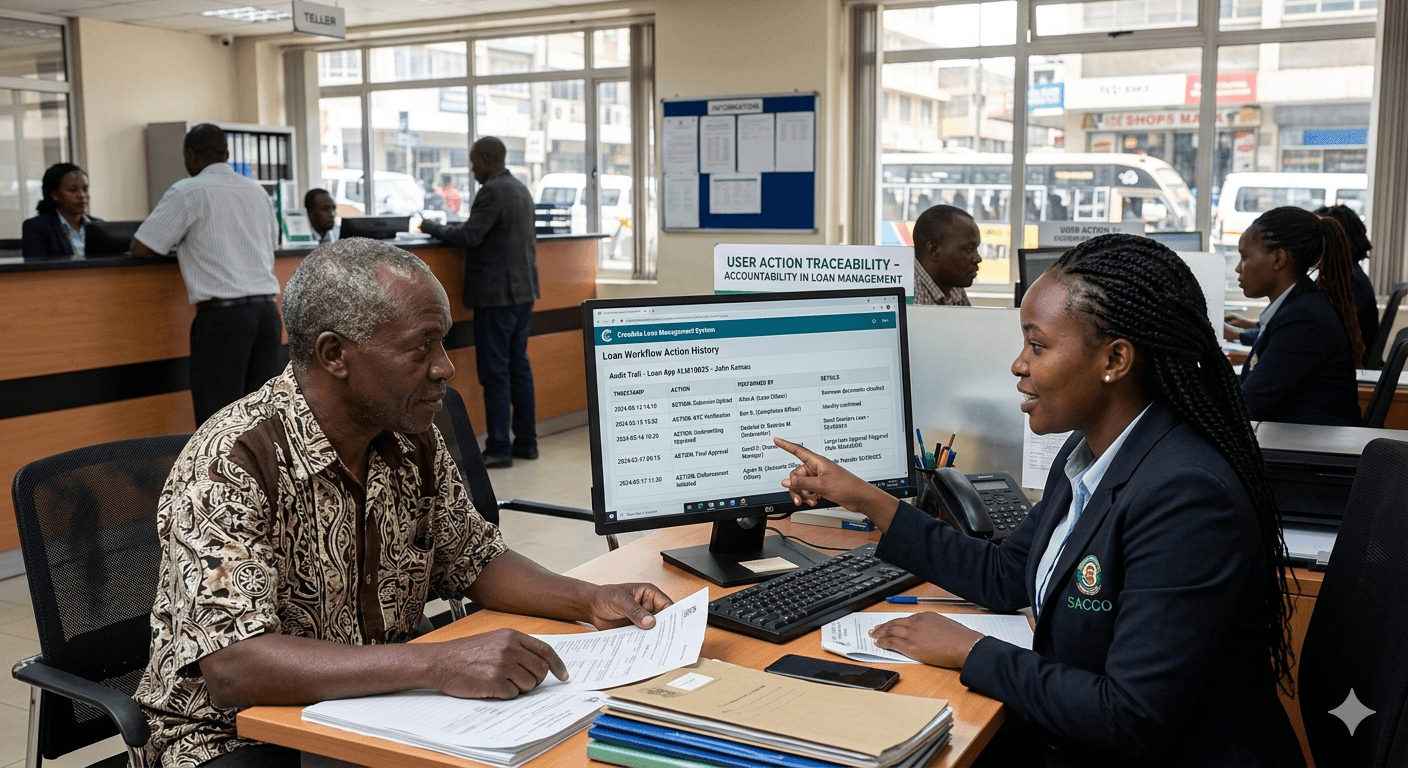

Once uploaded, documents move to verification. The SCCA carries out document verification and data capture as a discrete workflow stage, checking that each item is present, legible, certified where certification is required, and consistent with the captured application data. This separation matters: the people collecting documents at the front line are not the people who sign off that the documents are good. That maker-style separation, and the broader split-screen review where application details sit beside search and compliance results, is part of why the compliance checks in loan origination can be conducted against a verified, trustworthy file rather than raw uploads.

Verification is also where the documentary evidence is reconciled with the external checks. The pay slip and salary statements support net-pay verification — payslip net pay against bank-statement credits — while the ID supports IPRS verification and bio-data population, and the KRA PIN supports the tax-PIN check. Documents and compliance are two halves of the same assurance: the documents are the source, the checks confirm them against authoritative registers.

The auto-generated offer and OTP acceptance

Collecting documents is only half of the acceptance step. Once the documentation is in, WPB auto-generates a loan offer for the customer to execute and upload. This removes the manual drafting of offer letters and ensures the figures presented to the customer match the application as captured.

Acceptance is handled electronically through an OTP. The platform auto-generates a one-time password and sends it to the customer by SMS, together with a link to the loan and account-opening Terms and Conditions. The customer reviews the terms, and the OTP verifies their acceptance of those terms against the specific loan and account they are taking. Alongside this, two pieces of reference data are set automatically:

- A DSO code is auto-picked — the direct sales officer identifier attaching the application to the originating salesperson.

- A Reference Number is generated — the durable identifier the file carries through the rest of the workflow, into credit, booking and disbursement.

The most important control in this flow is what happens when something changes. Any amendment to customer or loan details after the OTP has been verified triggers a new OTP. A customer cannot accept one set of terms and then have the amount, tenure or particulars quietly altered behind that acceptance; the moment a material detail changes, the prior acceptance is invalidated and the customer must verify again against the revised terms. This keeps the signed offer and the booked loan in lock-step, and it gives the audit trail a clean record of exactly what the customer agreed to and when.

The Check-Off Authorization Form sits within this same document set. WPB auto-generates the Check-Off Authorization Form so the employer can be instructed to deduct repayments at source — the instrument that makes a check-off loan a check-off loan. For the wider scheme context in which that authorisation operates, see what check-off loans are and how they work in Kenya.

New to bank: parallel account creation

A new-to-bank applicant needs somewhere for the loan to be disbursed and the repayment to be operated, which is why the Account Opening Form appears on their checklist. WPB does not make the customer wait for an account before the loan can progress. Where the applicant is new to the bank, or an existing customer without an active account, a CIF and a transactional account are auto-created via API — on confirmation of check-offs or on approval — with the account type determined by income level. Crucially, this account opening runs in parallel with the loan workflow rather than blocking it.

This is the handoff between two distinct capabilities. The account-creation mechanics themselves are part of loan booking and disbursement through the core banking system, where the CIF, account and loan are all written into Finacle. The customer-onboarding depth — the data, the screening and the account-opening journey — is covered by the business account opening product. For a workplace-banking lender, the point to take away is that the document checklist flags the new-to-bank case, and the platform spins up the CIF and account alongside the lending workflow so disbursement is never held up waiting for an account number.

Why a structured document step pays off

Treating documentation as a structured, checklist-driven stage rather than a folder of scanned PDFs has compounding benefits down the line. The file that reaches credit is complete and verified, so analysts spend their time on the decision rather than chasing missing pages. The OTP-signed offer means acceptance is recorded electronically and re-verified whenever terms change, which closes a common gap between what was agreed and what was booked. The Check-Off Authorization Form and the buy-off loan statement are captured at source, so booking and any take-over settlement have the instruments they need. And because every upload, verification and OTP event is captured, the file is defensible after the fact — see how the audit trail and role-based access control hold the record together. For the full picture of how documentation fits the thirteen-stage journey, return to the workplace-banking complete guide.

Frequently asked questions

What documents does an existing customer need versus a new-to-bank customer?

Both groups need the core set: the Application Form and Terms and Conditions, a copy of the National ID or passport, the latest certified pay slip, the Employees Check-Off Authorization Form, a KRA PIN and a recent passport-size photograph. The main difference is salary evidence and the account. An existing customer whose salary already credits a Finacle account needs no stamped salary statements, and only needs an Account Opening Form if no account exists. A new-to-bank applicant must provide original latest three-month statements, stamped and signed, with a call-back to authenticate them, plus an Account Opening Form. Contract staff add a certified employment contract; expatriates add a letter of undertaking or work permit; buy-offs add the other lender's loan statement.

How does the customer sign the loan offer?

Once documentation is complete, WPB auto-generates a loan offer for the customer to execute and upload. Acceptance is electronic: the platform auto-generates a one-time password and sends it to the customer by SMS, together with a link to the loan and account-opening Terms and Conditions. The customer reviews those terms, and the OTP verifies their acceptance against the specific loan and account on offer. At the same time the platform auto-picks a DSO code, linking the application to the originating sales officer, and generates a Reference Number that the file carries through credit, booking and disbursement. There is no separate paper offer-letter exercise; the generated offer and the OTP acceptance form the signed record.

What happens if loan details change after the OTP is verified?

Any amendment to the customer or loan details after the OTP has been verified triggers a new OTP. The prior acceptance is invalidated, and the customer must verify again against the revised terms before the file proceeds. This control keeps the signed offer aligned with whatever is ultimately booked: a customer cannot accept one amount or tenure only to have it altered behind that acceptance. It also leaves a clean, time-stamped record in the audit trail of exactly what was agreed and when, which is valuable both for the credit file and for any later dispute. In practice it means the figures the customer saw and consented to are always the figures that move forward.

To see how the documentation and OTP-acceptance step fits the wider origination, booking and disbursement journey, explore the Workplace Banking platform or request a demo.