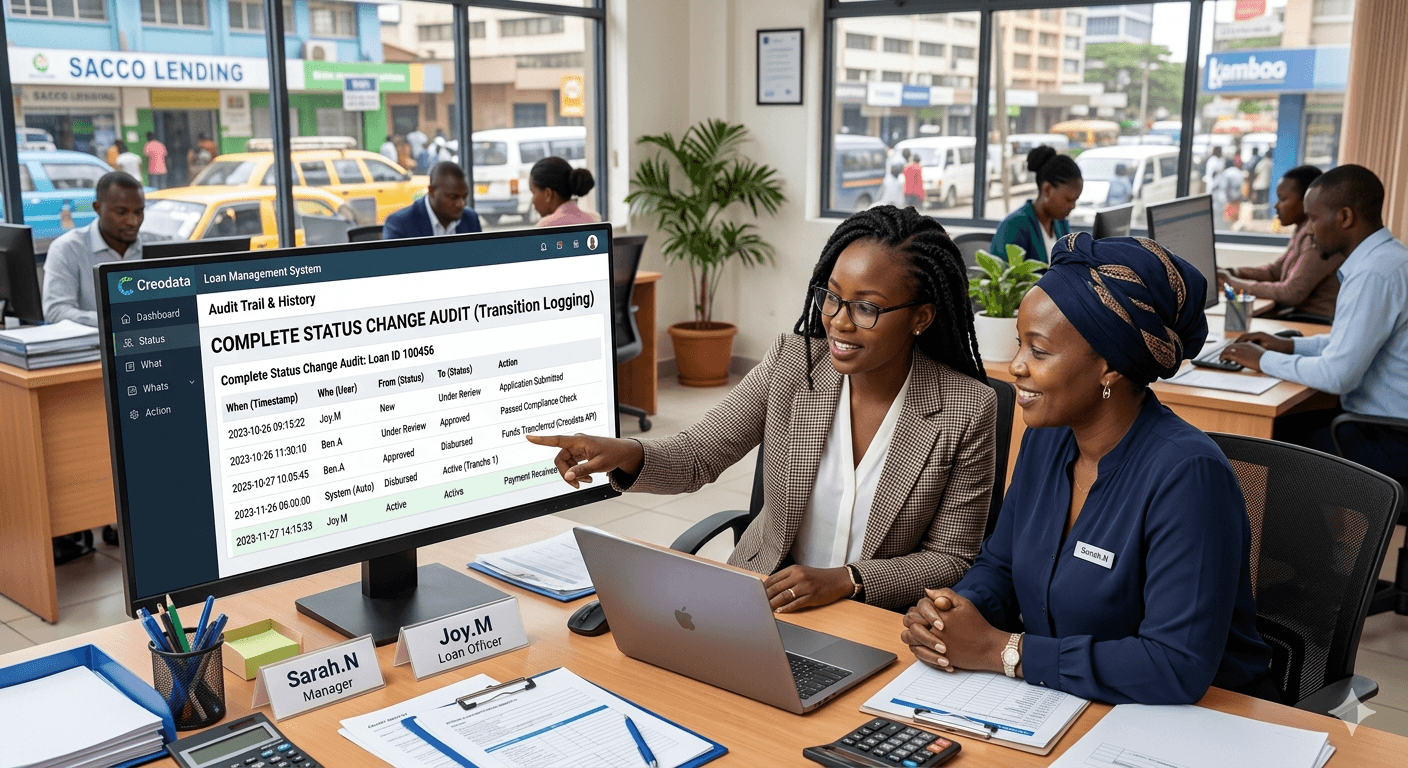

Complete Status Change Audit: Transition Logging in Audit Trail & History

Track every loan status transition with who changed what, when, and from which state—building accountability and compliance into your lending workflow.

In the world of lending, knowing precisely who changed what, when, and from what status to what status is not just a "nice-to-have" — it's vital. For lenders, auditors, compliance officers, risk managers, and microfinance institutions, this level of transparency is foundational for accountability, regulatory compliance, and operational clarity. In this article, we explore the concept of "Complete Status Change Audit", a use case for the broader category Audit Trail & History, with a focus on Transition Logging. We anchor the discussion around how such a feature can be implemented via a modern loan-management solution such as Creodata Loan Management, and highlight its advantages, purpose, and target users.

What Is "Complete Status Change Audit" (Transition Logging)?

A status change audit — or transition logging — refers to the mechanism within a loan-management system that records every change in the status of a loan (or loan application) over its lifecycle. That means:

- When an application or loan moves from one stage to another (for example: "New → Under Review → Approved → Disbursed → Repaid / Closed").

- Who initiated the change (which user, staff member, or automated process).

- When the change occurred (timestamp, date, time).

- From what previous status to what new status the loan/application moved.

Put simply: every transition is captured, logged, and becomes a permanent part of the audit trail for that loan. This ensures full visibility of the lifecycle of each loan application or loan — from first application to final closure.

Why is this critical? Because status changes reflect decision points, approvals, rejections, escalations, disbursements, repayments, restructuring, write-offs, closures, and more. Without a rigorous logging mechanism, it becomes nearly impossible to retrospectively analyze what happened, when and by whom — especially when multiple staff and multiple changes are involved.

How It Fits into Loan Management Systems: The Creodata Context

Creodata's Loan Management System (LMS) offers a robust, cloud-based lending platform that aims to cover the entire loan lifecycle — from onboarding through application, approval, disbursement, repayment, delinquency handling, and closure.

Key aspects where transition logging plays a natural role:

- The LMS supports configurable loan products, flexible approval workflows (multi-level, customizable), and multiple loan types.

- It offers "Audit Logging" as a core security & compliance feature — described as "comprehensive audit trails for all system activities and transactions."

- Given the customizable workflows and multi-step processes (application → approval → disbursement → repayment → closure), each stage transition can (and should) be logged to provide a full history of each loan or application.

In other words, while Creodata's public documentation may not always phrase it as "transition logging," the audit logging + workflow capabilities provide a solid foundation on which a "Complete Status Change Audit" can be built. Indeed, the same mechanisms that log user actions, system changes, and transaction history can be (and in a robust implementation, are) used to log status changes in loan applications/loans.

Advantages of Complete Status Change Audit / Transition Logging

Implementing transition logging for loan status changes yields several material benefits. Below are the key ones — and why they matter for lenders and financial institutions.

1. Full Visibility & Transparency

- With transition logging, lenders have an unbroken record of the entire lifecycle of each application/loan. There's no ambiguity about when a loan moved from "Under Review" to "Approved," who approved it, and when.

- Transparency extends to internal stakeholders (loan officers, risk & compliance, management) as well as external parties (auditors, regulators, oversight bodies). This helps demonstrate process integrity and fairness.

2. Accountability and Auditability

- In case of disputes (e.g., a client complains their loan was wrongly rejected, delayed, or mismanaged), the lender can trace back the precise history, seeing who made what decision and when.

- For internal governance and audit readiness, the logs provide evidence of compliance with internal policies, approval hierarchies, and regulatory requirements. Automated audit trails are crucial for regulatory examinations, internal auditing, or external compliance reviews. This is especially important in regulated finance sectors.

3. Risk Management & Operational Control

- Transition logging helps detect unusual or unauthorized changes (e.g., status jumps, repeated reversals, or unapproved status modifications). This can function as a deterrent against fraud, negligence, or operational errors.

- It supports robust risk-review workflows. For example, when dealing with large loans or high-risk portfolios, status changes like "pending collateral appraisal," "under risk review," "approved," "disbursed," can be tracked precisely, which is vital for lenders to maintain sound risk controls. Creodata already emphasizes audit logging and compliance readiness for large-loan review workflows.

4. Regulatory Compliance and Reporting

- Many regulators (central banks, financial authorities) require detailed records of loan decisioning, status changes, and audit trails. Transition logging ensures that lenders meet such compliance demands without relying on manual record-keeping.

- In jurisdictions where data protection, transparency, or financial regulations apply (e.g., anti-money laundering, consumer protection, IFRS accounting, provisioning rules), having an immutable audit/history of loan status changes provides confidence and simplifies compliance. Creodata's LMS is described as built with financial compliance in mind, aligning with frameworks like PCI DSS, GDPR, ISO 27001.

5. Operational Efficiency, Accountability & Workflow Optimization

- Having automated logging reduces reliance on manual spreadsheets, paper trails, or ad-hoc email chains to track status. This improves efficiency and reduces human error.

- Management, risk, and compliance teams can use logged data to analyze bottlenecks, approval delays, and process inefficiencies, enabling better process optimization and resource allocation.

- For institutions scaling operations — like small banks, SACCOs, or microfinance institutions — a transition-logging capable LMS helps them maintain institutional control as loan volume grows. Indeed, Creodata markets its LMS to small banks, SACCOs, and microfinance firms aiming to scale lending operations.

6. Dispute Resolution and Customer Trust

- From a customer perspective, especially in microfinance or member-based institutions like SACCOs, transparency builds trust. If a borrower queries delays, rejections, or status changes, the lender can provide a full history — making the process transparent and defensible.

- For lenders, this reduces reputational risk and potential litigation, as there is verifiable evidence for each action taken.

Why Creodata — and Who Should Use Transition Logging

Given the capabilities of Creodata's LMS — especially its audit logging, customizable workflows, cloud infrastructure, and compliance-ready design — a "Complete Status Change Audit" is a natural and powerful extension within their offering.

Who the Feature Benefits (Target Audience)

-

Small to Medium Banks – banks that may not have legacy mainframe systems or in-house IT infrastructure can deploy Creodata's solution on Azure and gain enterprise-grade auditability and workflow sophistication.

-

SACCOs and Credit Unions – member-based institutions needing transparent, auditable member-loan records to ensure fairness, accountability, and good governance. Creodata explicitly lists SACCOs among its target clients.

-

Microfinance Institutions (MFIs) – as MFIs scale and serve many small clients, managing multiple loan products, repayment schedules, and loan lifecycles — a complete audit trail becomes crucial for operational control and regulatory readiness.

-

Risk & Compliance Teams – internal compliance officers, risk managers, external auditors, regulatory examiners who need full visibility into loan decisioning and status changes.

-

Operations / Back-Office Teams – staff managing loan operations, approvals, disbursements, repayments — transition logging gives them clarity, reduces manual bookkeeping, and helps in process audits and optimization.

-

Senior Management & Executive Leadership – for oversight, control, and governance: being able to audit, report, and analyze loan lifecycle data helps in strategic decisions, risk assessment, and regulatory reporting.

-

External Auditors / Regulators / Legal-Compliance Entities – who may request evidence of proper procedure, decision chronology, or data integrity during compliance checks or investigations.

Conclusion

In a lending environment — especially for small banks, SACCOs, microfinance institutions, and growing financial organizations — transparency, compliance, and operational control are non-negotiable. A feature like "Complete Status Change Audit" (Transition Logging) moves an institution from relying on manual or ad-hoc record-keeping to having an automated, auditable, and reliable history of every loan's journey.

By integrating transition logging into a loan management framework like Creodata's, institutions can confidently:

- Demonstrate compliance and governance

- Trace decisions and status changes back to the responsible parties

- Provide evidence during audits, disputes, or regulatory reviews

- Gain operational insights to optimize processes

- Build trust with customers, members, investors, and regulators

Whether you are a small SACCO, a microfinance institution, or an emerging bank in Nairobi, Nairobi County (or anywhere else), implementing a robust "Complete Status Change Audit" mechanism helps ensure that your lending operations are transparent, efficient, and future-proof.

For more information, visit Creodata.com